A crisis operator working for banking industry solidarity

The FGDR's mission is to intervene in crisis management, at the request of the supervisory authorities of the banking and financial sector, either upstream, before the crisis occurs or, when necessary, downstream, if the crisis has already occurred, by compensating customers.

At 31/12/2025, it covered 1134 member institutions with one or more of its three mechanisms: the deposit guarantee scheme, the investor compensation scheme and the performance bonds guarantee scheme.

- Fulfilling this mission entails, at the legal and operational levels, developing specific tools and making them available over the long term to all banking and financial sector operators.

- The FGDR's activity also has an international dimension, since its regulatory framework derives largely from European texts. Exchanges with other European and international deposit schemes are a key factor in terms of performance, planning and progress.

The FGDR: a player that has seen profound changes since the 2008 crisis

The financial crisis that began in 2008 led authorities to strengthen financial crisis management tools. In 2009, the European Union decided to reduce the compensation period for customers of a failed bank to 20 working days, and then to seven days in 2014.

The FGDR set out to address the consequences of this new requirement and radically change its method of operation; indeed, paying compensation within seven working days requires processes to be developed up front with all financial institutions to ensure the rapid collection and processing of all the data needed to compensate a large number of depositors with a wide variety of situations. Together with all the sector's operators, it created appropriate data standards known as "Single Customer View files".

It worked with the public authorities to define the new regulations.

To increase its operational capacity to manage these new challenges, it developed its IT resources, expanded its teams and signed contracts with a growing number of external partners. Once this new model had been built, it also entered a maintenance phase: regular annual controls of each credit institution’s operational capacity were set up, while the FGDR itself made a commitment to conduct stress tests to ensure its operational capability at all times.

It has also focused on bank customers by implementing an active communication policy. Lastly, it has searched for best practices worldwide and shared its own experience with its counterparts.

Today, the FGDR has a robust deposit guarantee compensation system that undergoes regular and increasingly in-depth testing.

Relations with member institutions

All companies that receive a licence from the Prudential Supervision and Resolution Authority (ACPR) to operate as a credit institution, an investment services provider or a financial intermediary authorised to issue regulated performance bonds are members of the FGDR under the deposit guarantee, investor compensation or performance bonds guarantee schemes, respectively. This membership is mandatory and a prerequisite for conducting business in France.

All financial institutions that fall within the scope of resolution at the national level, and are therefore contributors to the National Resolution Fund, are also members of the FGDR.

At 31 December 2021, the Fonds de Garantie des Dépôts et de Résolution had

472 members,

many of which participate in several schemes.

Taken separately, each mechanism currently has:

- Deposit guarantee scheme: 323 members;

- Investor compensation scheme: 289 members;

- Performance bonds guarantee scheme: 252 members;

- Guarantee of services provides by asset management companies :684 members ;

- National Resolution Fund (NRF): 87 members.

A scheme fully financed by its members’ contributions

- The FGDR collects contributions from its members. It receives no public funding. These are annual contributions determined in accordance with the applicable regulations.

- The ACPR sets the general rules for calculating contributions, after obtaining the opinion of the FGDR's Supervisory Board. The FGDR's Supervisory Board, for its part, determines the level of contributions each year after obtaining the assent of the ACPR, and that of the Financial Markets Authority (AMF) for the investor compensation scheme.

-

Contributions

take into account factors relating to the basis of calculation (amount of covered deposits, volume of securities portfolios, amount of performance bonds), on the one hand, and each member institution's specific risk factors, on the other. For the deposit guarantee scheme, the total amount of resources available to the FGDR for its interventions is within the range defined by the European texts by the year 2024, between 0.5% and 0.8% of covered deposits.

The “Integrated Compensation and Communication System” (CCS)

To build the new compensation tools and processes, in 2011 the FGDR, working closely with French banks, launched an extensive project called the “20-Day Project” (which later became the “7-Day Project” with the new 2014 standards). This project was structured into two major parts:

- Technical production of the “SCV File” by banks.

Banks must, at their own responsibility, identify customers and their deposits (eligible or ineligible), calculate their positions at the date and time (D/T) at which the unavailability of deposits is declared by the ACPR and send them to the FGDR within two days of the unavailability of the deposits. This obligation is fulfilled by uploading a standardised "Single Customer View" (SCV) file, the production of which is subject to annual control by the FGDR;

- The end-to-end processing platform called the “Integrated Compensation and Communication System”. For the FGDR, the project's general architecture is structured around a core computing solution and related services required for the proper operation of this solution: management of payment means, telephone call centre for depositors, digitisation and archiving, processing centre for complex compensation cases, Secure Compensation Area and press relations centre.

Work related to “7-Day Communication”

In the event of a banking crisis, it is crucial that the communication campaigns launched by the FGDR and the public authorities, on the one hand, and by the failed bank, on the other, are coordinated so as to ensure the successful management of the financial crisis and to put an end to any media crisis that may arise.

Since 2015, the FGDR has had a financial working group to deal specifically with customer information and communication, both under normal circumstances and in case of compensation. Following several projects focused on implementing the new 2015 regulations on customer information, the group worked on developing a process to coordinate communication between the FGDR and a member institution in the event of the institution's failure, which resulted in three new initiatives:

- the appointment of a “Crisis Communication” correspondent for the FGDR within each member bank;

- the launch, along with these correspondents, of an exchange of information about the communication systems in place and the resources to be activated in case of the FGDR’s intervention;

- the drafting of a communication procedure guide to help coordinate the institution's communication with that of the FGDR.

Relations with the banking and financial sector

To carry out its mission, the FGDR regularly invites banking sector operators to participate in working groups.

- Recurring plenary meetings with members are an important way of staying in touch with the banking industry. They focus on work related to the Compensation and Communication System (CCS), regular controls of Single Customer View files and communication with depositors. These meetings take place due to the active support of the Fédération Bancaire Française (FBF) and the Office de Coordination Bancaire et Financière (OCBF).

Relations with the public authorities

Created by law with a mission to serve the public interest and reinforced by public oversight, the FGDR is a private body with a governance that comes from the financial sector.

The Chairman of the FGDR's Executive Board receives a specific authorisation from the Minister for Economic Affairs and Finance, who appoints a non-voting member who participates in the work of the FGDR's Supervisory Board. This model keeps the FGDR close to both financial operators and the public authorities.

Financial stability and customer protection are a common goal, shared by the public authorities and by private players, in which everyone has a role to play.

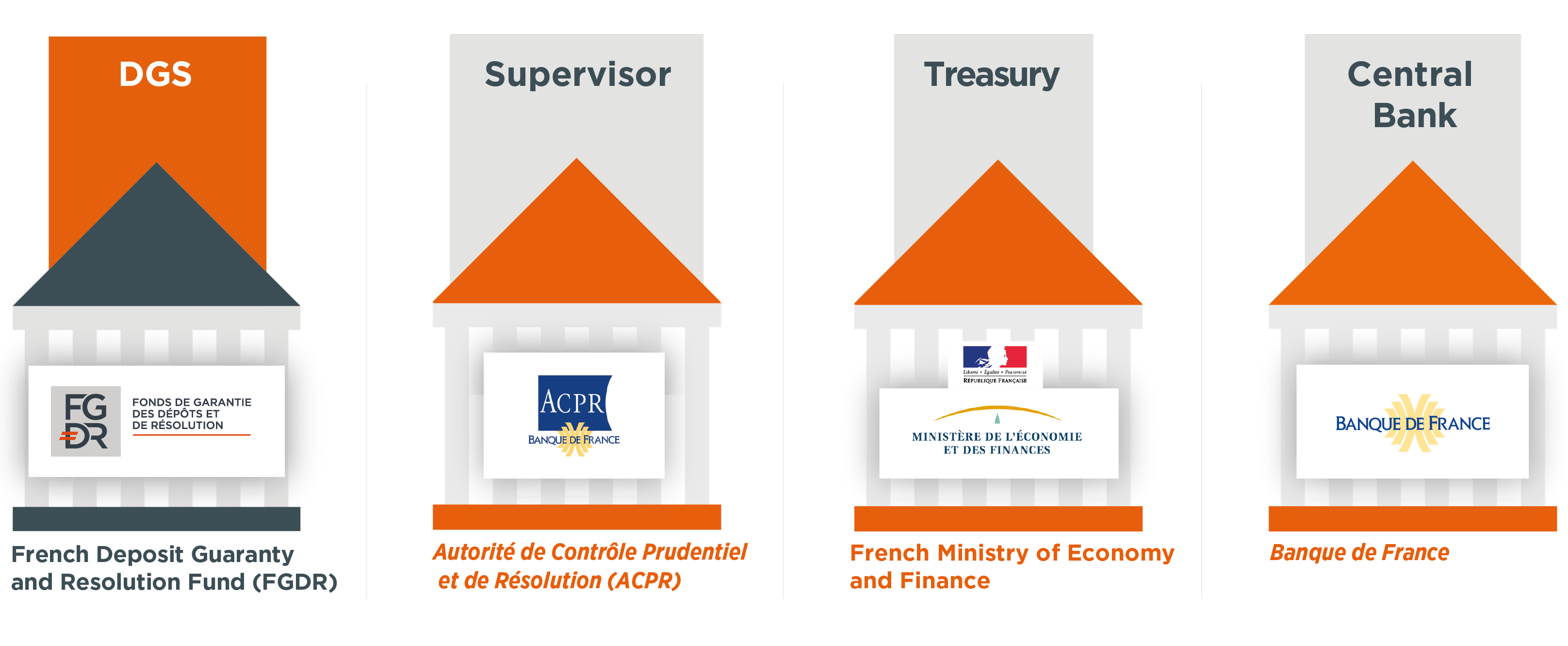

The “financial safety net”

The five main participants in the financial safety net responsible for managing a potential banking and financial crisis are:

- the Prudential Supervision and Resolution Authority (ACPR), which provides supervision and, as a resolution authority, is responsible for the resolution process;

- the Financial Markets Authority (AMF), which regulates the financial markets and savings products;

- the Banque de France , lender of last resort;

- the State guarantee, ultimate guarantor of the system;

- and the FGDR, the crisis operator.

The ACPR is the authority appointed to supervise the deposit guarantee scheme.

Only the ACPR can initiate an intervention by the FGDR based on its determination of an institution's probable or verified failure.

The FGDR, member of the Collège de Résolution

Crisis management requires close coordination among the players, which is made possible by regular contacts and specific bodies such as the High Council for Financial Stability (HCSF) at the macro-prudential level and the Collège de Résolution at the individual institution level. The FGDR participates directly in the Collège de Résolution, which is chaired by the Governor of the Banque de France and overseen by the ACPR.

Relations with the general public

The FGDR's mission is to inform customers of the financial sector about the guarantees available to them. Doing so is essential to strengthening confidence in the financial sector. This is why, for many years, the FGDR has increasingly published educational and interactive information aimed at the general public and banking and financial sector customers.

In this way, the FGDR can best fulfil its role of crisis operator in support of financial stability, both under normal circumstances and in times of crisis.

Inform as many people as possible about the deposit guarantee scheme

The “DGSD2” Directive adopted on 16 April 2014 (2014/49/EU) and its transposition into French law brought significant improvements in terms of information provided to depositors. Banks now provide more detailed information about the deposit guarantee scheme to their customers in the following ways:

- by giving an information notice about the deposit protection scheme to prospects who are considering opening a new savings or other account covered by this protection;

- by having all customers sign this notice when they open a new savings or other account which is covered;

- by sending this notice to each customer once a year;

- by including the words “protection by the deposit guarantee scheme” on the periodic statements of protected savings and other accounts.

In accordance with these same regulatory requirements, the FGDR provides the public with educational information about the guarantees available to customers of banks and financial institutions through the media, its website and, more recently, social networks.

Relations with international partners

Interaction with international partners is a core aspect of the FGDR's activity. In fact, most of the regulation governing financial crisis management and customer protection tools is developed within the European Union and at the international level.

By definition, all crisis operators intervene only sporadically. It is crucial that they share their experiences and exchange information about the tools they use and the way in which they apply common rules.

Work within the EFDI

The European Forum of Deposit Insurers (EFDI), of which the FGDR was a founding member in 2002, brings together all European deposit insurers, including those outside the European Union.

Through its chairmanship, the FGDR has managed the EFDI since September 2016, giving the French guarantee scheme a greater role than ever in the European and international dimension of deposit insurance.

The EFDI's roadmap covers, in particular:

- scheduling and conducting stress tests (Stress Test Working Group);

- relations with the public (Public Relations and Communication Committee);

- research work (Research Working Group – risk-based contribution systems, changes in covered deposits, etc.);

- cooperation among investor compensation schemes (Investors Compensation Scheme Working Group);

- a specific programme for the European Union's deposit guarantee schemes (EU Committee).

The EFDI’s work priorities - EU Committee

The EU Committee’s activity is currently centred around three important work priorities for the collective practice and consideration of the European Union’s deposit insurers.

- The “D2I” initiative (DGSD Implementation Initiative) is working on a complete review of the implementation of the 2014 DGSD2 Directive.

The publications of the EFDI’s EU Committee at efdi.eu/news :

Non-Binding Guidance:- Compensation within seven days;

- Investment policies;

- Alternative resources;

- Complex compensation;

- Preventive and alternative interventions.

- The Banking Union Working Group is examining the feasibility and technical procedures for applying the objectives of the Banking Union. The Technical considerations for the design of EDIS (EFDI - November 2018)

- The Cross-Border Working Group is responsible for harmonising and strengthening cooperation among guarantee schemes in the event of cross-border compensation. Its work is based on the Multilateral Cooperation Agreement, prepared by the EFDI in 2016 and approved by the European Banking Authority (EBA), which defines the technical terms of cooperation.

The Multilateral Cooperation Agreement (EFDI – September 2016)

The EBA’s work

The European Banking Authority (EBA) was created in 2011 to strengthen the European system of financial supervision. It is active in both banking and deposit insurance. The EBA’s work encompasses the European Union's deposit guarantee schemes.

The EBA’s task force, known as “TFDGS”

This task force, which brings together the EU's public authorities and guarantee funds, serves as a platform of cooperation on the technical and operational aspects of the deposit insurance activity. Both the FGDR and the ACPR have been actively involved in it since its creation.

The “TFDGS's” roadmap:

- prepare for potential changes to European regulations on deposit insurance in the future;

- review the terms of implementation of the European Directive on deposit guarantee schemes (DGSD2) with respect to all its aspects: eligibility, coverage, cooperation among schemes, anti-money laundering, compensation process, resources of the guarantee schemes and use of such resources;

- identify and analyse the stress test methods used by the deposit guarantee schemes in order to develop a more organised framework and assess their performance.

The IADI’s work

The International Association of Deposit Insurers (IADI) brings together most of the world’s guarantee schemes. Its mission is to increase the effectiveness of deposit insurance worldwide through the issuance of guidelines and through international cooperation among deposit insurers.

In particular, the IADI issues the “Core Principles for Effective

Deposit

Insurance Systems”, which constitute the basic doctrine of all deposit insurers, as well as the standard used by the International Monetary Fund (IMF) as the basis for the periodic assessments of the Member States’ national financial sectors and regulation.

|

The IADI Core Principles (November 2014) In line with the Core Principles, the IADI issues research and guidance papers for deposit guarantee schemes on many issues related to their activity:

The association also develops technical cooperation initiatives to help its members assess and improve their effectiveness in terms of deposit insurance. The FGDR, a founding member of the IADI, also serves on the association’s Executive Committee and is actively involved in its working groups and committees. |